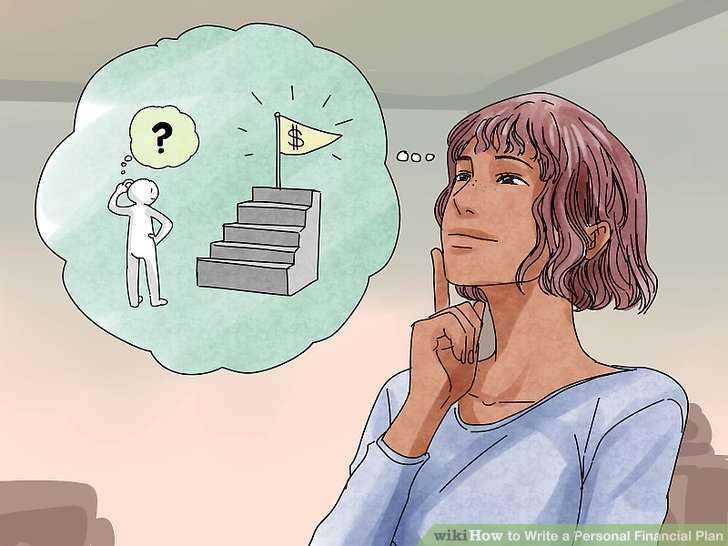

Set Financial Goals

A clear set of goals can keep you motivated and help you plan to reach it faster.

Have different goals for what you want to achieve in the next 3-months, 1 year and 5 years. This way you'll have some short and long-term goals to look forward too.

4.76K

19K reads

CURATED FROM

IDEAS CURATED BY

"There's no money in poetry, but then there's no poetry in money, either." ~ Robert Graves

These are pretty basic but we would all be far ahead financially if we did a few of them.

“

The idea is part of this collection:

Learn more about moneyandinvestments with this collection

The importance of networking in podcasting

How to grow your podcast audience

How to monetize your podcast

Related collections

Similar ideas to Set Financial Goals

Identify Your Goals

Once you make a decision, identify your long- and short-term goals . This helps to chart a course toward eventually landing work in your chosen field.

- Long-term goals typically take about three to five years to reach, while you can usually fulfill a short-term goal in six months t...

Setting Goals

- Focus on one domain at a time.

- Write down your goals. This makes you more likely to take action.

- Goals should be SMART: specific, measurable, attainable, realistic and time -bound.

- Set a combination of immediate, short term (days to weeks), medium term (weeks to month...

Set concrete goals

To become successful sooner, you first need a road map for your career. What do you want to achieve in your career?

Long term goals help you create a framework for your career. With them in mind, create smaller goals. Set the bar high to ensure you always have a source of motiva...

Read & Learn

20x Faster

without

deepstash

with

deepstash

with

deepstash

Personalized microlearning

—

100+ Learning Journeys

—

Access to 200,000+ ideas

—

Access to the mobile app

—

Unlimited idea saving

—

—

Unlimited history

—

—

Unlimited listening to ideas

—

—

Downloading & offline access

—

—

Supercharge your mind with one idea per day

Enter your email and spend 1 minute every day to learn something new.

I agree to receive email updates