Facts about Money, Cash, Credit & more

The web is teeming with information on finance and money management strategies, yet it's the quirky, fun facts about money and the principles behind saving and spending that truly resonate. The real magic lies in finding out cool and interesting facts about money, brought to life through the shared knowledge of a community. Deepstash offers a compilation of finance fun facts, insights, and trivia on money, gathered from the collective experiences of individuals who have read through books, articles, podcasts or articles on financial planning, budgeting, and saving. Here, you'll discover not just random facts about money but genuine nuggets of wisdom that have proven their worth in real-world financial management across various life phases.

Discover 5,000+ Money Facts & Financial Insights from Curated Sources

Immerse yourself in a groundbreaking way to learn about money through Deepstash's innovative microlearning platform, specializing in the fun and fascinating aspects of finance. Explore quick reads and flashcard-like snippets that distill the essence of financial wisdom, from budgeting and saving tips to investing secrets and beyond, captured in "articles" and "journeys." These compact insights serve as a vast reservoir of finance facts for beginners, students, millennials, and anyone eager to boost their financial IQ.

Uncover Simplified Finance Facts with Our Flashcard-Like Insights!

Core idea curated from:

Budgeting = creating a plan to spend your money

Budgeting is simply balancing your expenses with your income.

It's a plan for the coordination of resources and expenditures. When you budget your money, there’s a desired outcome. And being able to track your spending should ultimately move you in the right direction towards meeting your financial goals.

2.2K

Core idea curated from:

How to create a budget

- Gather Some Financial Information: gather a detailed list of your income and expenses.

- Select a Budgeting Method: figure out how you’ll budget your money to meet your most pressing financial goals.

- Create Your Budget: tally up all your expenses and income to see where you stand and allocate expenses.

- Execute Your Plan: you can use a notebook, pen and paper, a spreadsheet or an online software.

- Reward Yourself: you can work a small percentage into your budget to treat yourself each month.

2.49K

Core idea curated from:

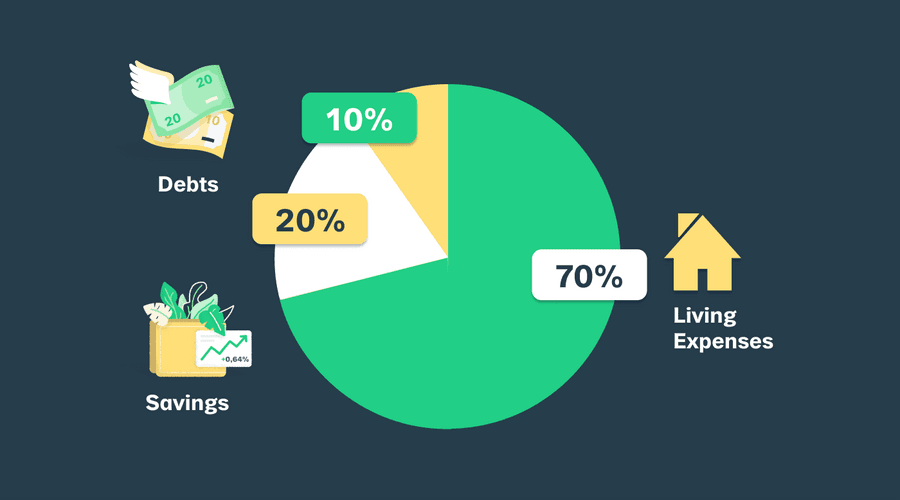

The 70:20:10 budgeting method

This method suggests that you allocate 70 percent of your income to expenses, 20 percent to savings, and the remaining 10 percent to debt.

70:20:10 may work for someone with a healthy emergency fund and minimal debt.

2.62K

Core idea curated from:

The 50:30:20 budgeting method

Under this method, 50 percent goes to expenses, 30 percent goes to wants, and 20 percent goes to a combination of debt and savings.

A person with a healthy amount of disposable income but loads of debt could probably benefit more from the 50:30:20 method.

2.53K

Core idea curated from:

Making Your Budget Too Strict

Budget for the life you have. When you’re going through your budget and assigning spending categories, be realistic.

Don’t tell yourself you’ll never buy a single discretionary item, because you’re setting yourself up for failure. Give yourself some breathing room.

370

Core idea curated from:

Budgeting for a Life You Can’t Afford

This becomes a problem when you’re spending for a life you can’t afford. It puts pressure on your budget and encourages you to live in a paycheck to paycheck cycle.

Assess your financial situation, cut back on your expenses, prioritize your money goals, and then come up with a new spending plan.

334

Core idea curated from:

Budgeting Without a Purpose

It’s hard to stick to a budget that doesn’t have a goal.

When there isn’t one, your budget becomes an afterthought rather than a spending plan to reach your financial goals.

343

Core idea curated from:

A Monthly Budget For Your Money

No matter how little or how much money you earn, creating a monthly budget is one of the most important aspects of managing your finances. What gets measured gets managed.

Having a budget doesn't stop you from spending money the way you want it to, but works like a partner to track your spending and allocating resources to help you reach your financial goals.

1.66K

Core idea curated from:

Being Frugal Is Not Cheap

Frugal people do spend money, but want the maximum bang for the buck, without stressing themselves.

Frugality does not mean compromising quality, neglecting your social life, or being a cheap stake. It is about making smart spending choices, like buying second-hand clothing, avoiding pricey subscriptions or brands.

218

Core idea curated from:

Be A Smart Spender

- Use tools like financial books, podcasts, and online savings groups.

- Avoid indulging in unnecessary expenses daily, reducing them or finding healthier and more affordable alternatives.

- Cultivate a healthier attitude and the right mindset towards your finances.

- Know that small, practical, money-saving actions can compound into better living for you in the long run.

219

Core idea curated from:

Understanding recessions are vital

Recessions are part of the fabric of a dynamic economy. The average investor fears recessions because they mean lower home prices, lower stock prices, and less or no work.

Several things can cause, or worsen, a recession — soaring interest rates, or ill-conceived legislation. If you understand recessions, you will have many opportunities to look forward to when the recession ends.

139

Core idea curated from:

The best time to buy stocks

Historically, the best time to buy stocks is when the NBER announces the start of a recession.

The NBER takes at least six months to determine if a recession has started. The average post-WWII recession lasts 11.1 months. By the time the bureau announces a recession, it is nearly over. Often investors are quicker to spot the beginning of recovery long before the NBER does.

156

Core idea curated from:

Spending your money

The best thing to do with your money during a recession is to pay off your credit card debt.

Paying off a credit card that charges 18% interest is equivalent to getting an 18% return on investment. You may not get that from most other investments during a recession.

141

Core idea curated from:

Measuring well-being: people vs money

The turn toward financial statistics means that instead of considering how economic developments could meet our needs, it instead is to determine whether individuals are meeting the demand of the economy.

Until the 1850s, social measurement in 19th-century America was a collection of social indicators known as "moral statistics," which focused on the physical, social, spiritual, and mental conditions of the people. Human beings were at the center, not dollars and cents.

207

Core idea curated from:

The Never-Ending Anxiety Of Making Money

Modern life is filled with the never-ending anxiety of making money. Our approach right from the school days is to earn money and accumulate the things required in society.

It is a powerful cultural force that makes us accumulate stuff, and is not as practical as it is emotionally and psychologically significant. A failure to make money is considered irresponsible, and a poor person who is not earning is shunned in today’s society.

31

Core idea curated from:

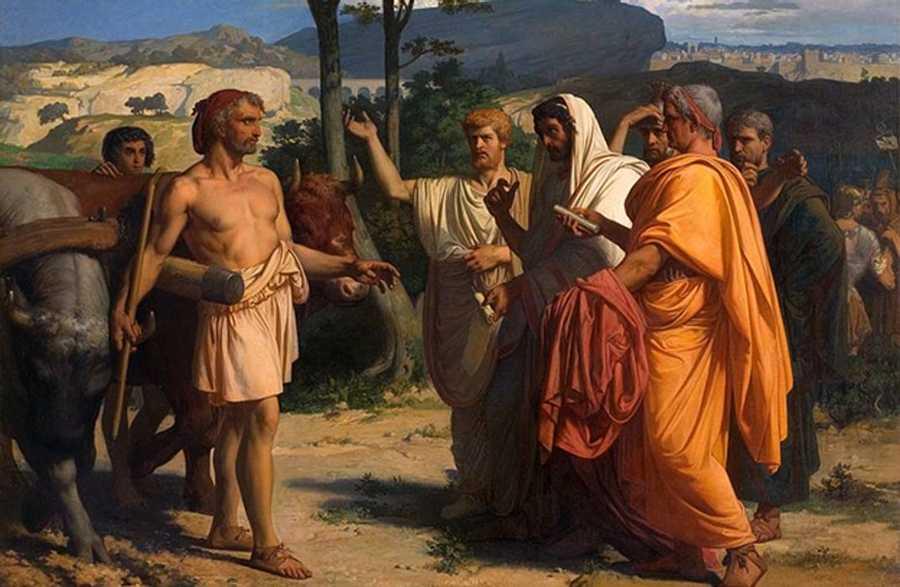

Voluntary Poverty: Forgoing The Pursuit Of Wealth

History shows us plenty of examples of people pursuing goals that are not towards earning wealth.

The Roman statesman Lucius Quinctius Cincinnatus had a successful public career but made no money, even though he came from an impoverished family. There are many such examples from India, where learned and creative individuals chose to live an impoverished life.

29

Core idea curated from:

Our Preoccupation With Money

Chasing money is in a way proof that one hasn’t found the real reason for being alive. We haven’t identified a passion that could replace the concept of earning a livelihood from our minds. Wealth is tied to prestige, respect and social status and the thought of becoming untethered from our ‘network’ is a thought akin to dying.

If we focus our lives on what matters to us authentically, then we will fall out of this romance with dollar bills, and get into our passions, which require little or no money.

36

Core idea curated from:

Bitcoin was born from a crisis

In the middle of the 2008 banking crisis, a group of anarchists, libertarians, and other tech-savvy true believers created digital cash.

In August 2008, bitcoin dot org was registered as a domain. On Halloween the same year, Satoshi Nakamoto put up a whitepaper describing a decentralised system of electronic transactions that did not involve a financial institution.

71

Core idea curated from:

Money is a value token

Bitcoin highlights how fundamentally bizarre money is. Money is a value token that makes exchange easier. It isn't real in a tangible way. But it's real enough that people fight and die for it.

Bitcoin's ideology is that of a specific distrust of financial institutions. In 2009, many people were looking for alternatives to the mainstream financial system that had disastrously failed. Bitcoin was the first successful attempt for an alternative financial system.

65

Core idea curated from:

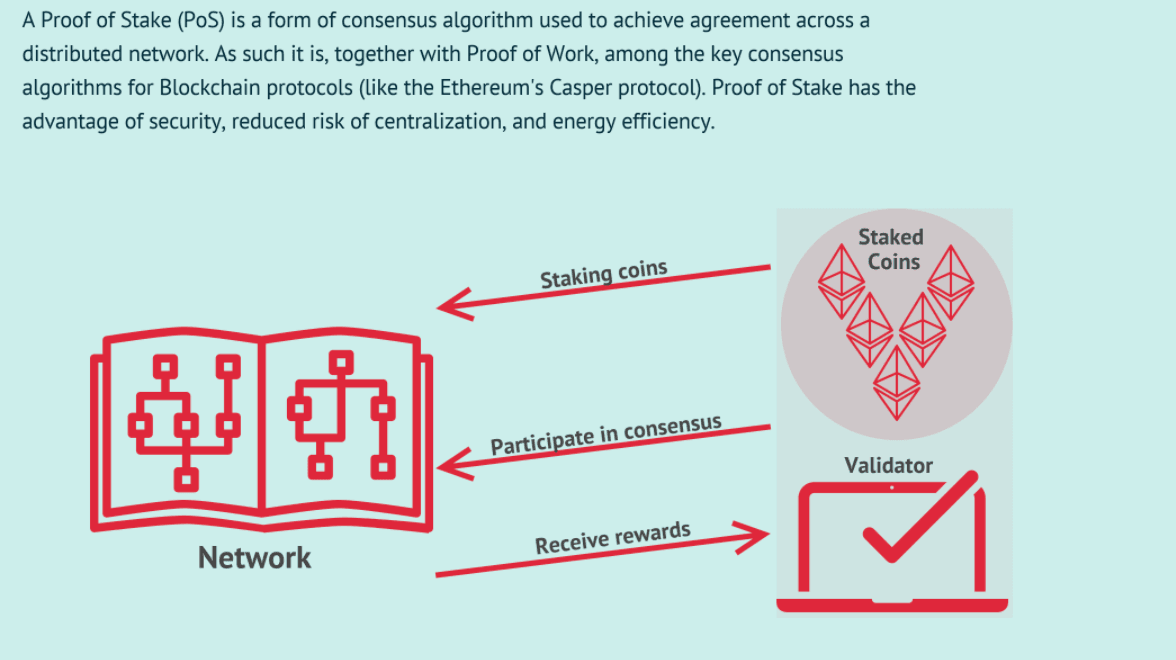

Ethereum promise

Ethereum's initial success can be attributed to a few elements. Ethereum is programable, meaning apps can run on the Ethereum blockchain. This is what let to Ethereum being used in:

- Decentralised Finance, or DeFi, meaning that apps like investments, insurance etc can be run without a central authority.

- NFTs, tokens to prove the authenticity and ownership of an object (digital or physical)

- The consensus in the network through proof of stake. New coins are created by putting guaranteeing your existing money. This incentives people to be good actors and decreases the money supply, increasing its price.

30

Core idea curated from:

Fiat money

Fiat money is a government-issued currency that is not backed by a commodity such as gold. Most paper notes started as being backed by a reserve of valuable commodities, usually gold (the "Gold Standard"). Tying a currency to gold limits inflation and money supply.

But politicians hate the gold standard, so since Nixon's presidency, the US dollar was no longer tied to gold and money had value just because the government says so.

49

Core idea curated from:

A history of the US fiat currency

1933 - President Franklin D. Roosevelt had gold confiscated and people were forced to accept paper money for their gold. The government needed people to adopt the inflated paper and they used force.

1940s - Bretton Woods Agreement created a collective international currency peg to the U.S. dollar which was in turn pegged to the price of gold.

1971 - President Nixon unilaterally cancelled the direct international convertibility of the US dollars to gold. Making the US government in charge of money supply and world money master.

41

Core idea curated from:

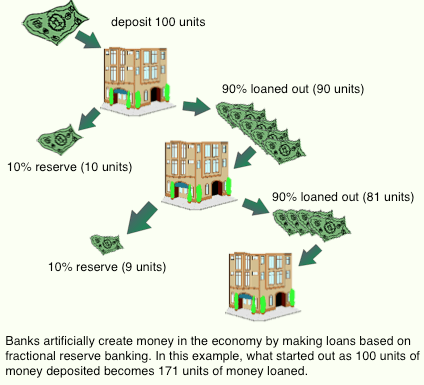

Fractional Reserve & Money Supply

Banks loan money they don't have. Most hold a limited reserve to serve the few who decide to make redraws. When the majority decides to liquidate their bank accounts we have what is called a bank run.

In order to protect the banks, central banks were created to provide a guaranteed reserve for commercial banks. But once the government stepped in to protect the banks the fractional reserve mandates(only a fraction of deposits are backed by actual cash) began to be used to make up the money from thin air. Every dollar that a bank holds can be multiplied by at least 10x.

38

Core idea curated from:

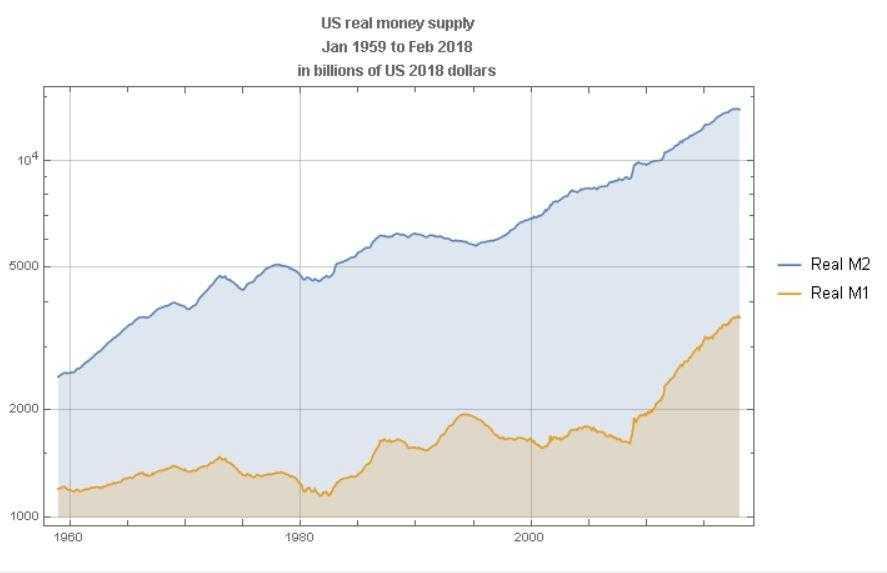

Money Supply & Inflation

We can measure the supply of money that exists in the market with main metrics:

- M1 money supply includes liquid money aka cash.

- M2 (which includes M1) includes loans, deposits & market funds. This is mainly made up money.

As the chart shows the US (and all other countries with central banks) have most of the monetary mass made up. An influx of money causes inflation and this is exactly what during the last decades.

43

Core idea curated from:

We print money digitally. As a central bank, we have the ability to create money. And we do that by buying bonds for other government guaranteed securities. And that actually increases the money supply. We also print actual currency and we distribute that through the Federal Reserve banks.

JAY POWELL, CHIEF OF FEDERAL RESERVE

40

Core idea curated from:

Tripple point money

Robert Greer says that there are three asset superclasses:

- Capital Assets are productive & generate value or cash-flow: equities, bonds, or rentable real estate.

- Transformable/Consumable Assets: can be consumed one time, transformed into another asset, and their consumption produces economic yield: energy or commodities.

- Store-of-Value Assets are scarce, cannot be consumed, just transferred, and their value persists over time and space: gold, currencies, art, or bitcoin.

68

Core idea curated from:

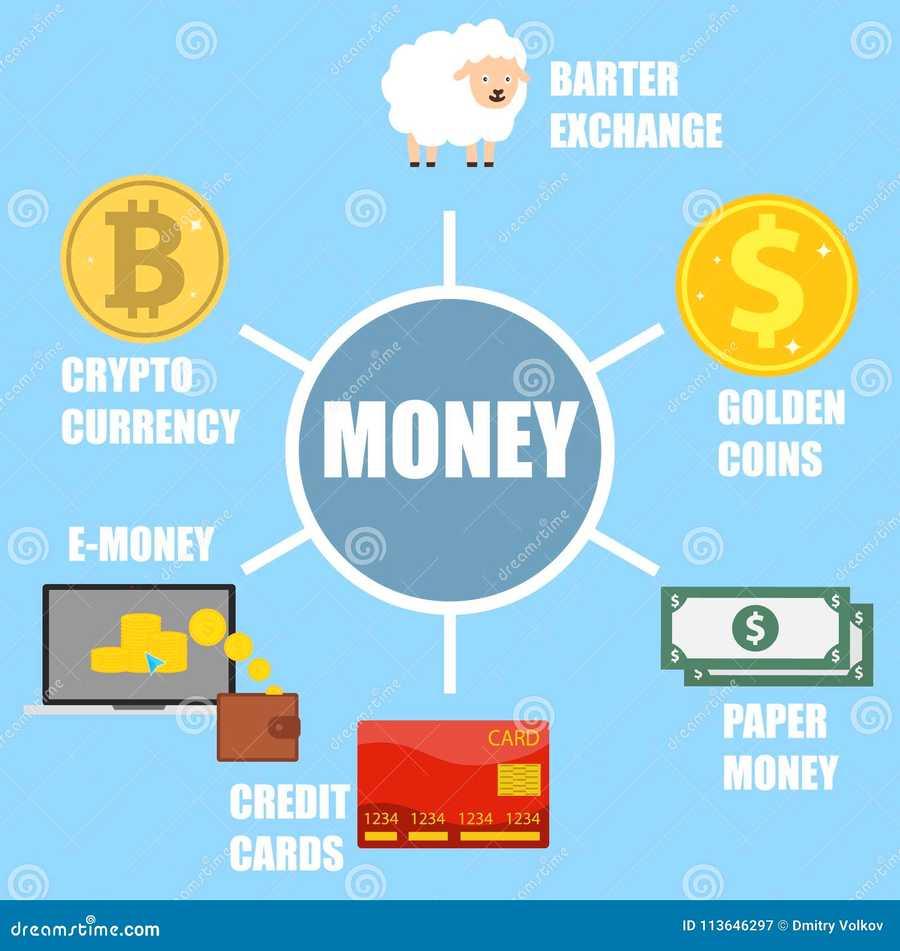

What is money?

Money is a WIDELY ACCEPTED medium of EXCHANGE. Lets analyse each word, they really have a huge importance:

- Widely: it has to be accepted by many people, otherwise it can’t work.

- Accepted: It has to be accepted by all these people, which means we need to have some sort of agreement that we will all accept it.

- Exchange: Now that everyone accepts it, we also agree that it has some sort of value and we can exchange it for certain things.

747

Core idea curated from:

Why is money valuable?

The reason money is valuable is because we all have FAITH in it, and this faith is operating in present and future times.

Think about it, the reason we believe in money is because we know that if we save some amount of it, we can use it in the future to buy something as this money will still have value, right?

709

Core idea curated from:

Countries currencies used to be backed by gold long ago

Countries currencies used to be backed by gold long ago, nowadays they’re only backed by governmental policy so we could agree that:

- Good government equals to: good monetary policy and valuable currency

- Bad Government equals to: bad monetary policy and currency losing value

- Communist dictatorship equals to: no policy, just theft and the country’s currency becomes worthless and destroyed

710

Core idea curated from:

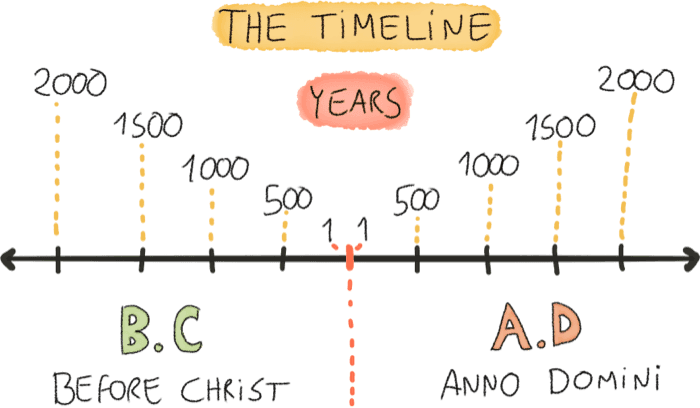

The Timeline we’ll use for the History of money

In case you’re not familiar, this is the timeline of history we’ll be using.

- BC stands for: Before Christ

- AD stands for: Anno Domini

It can get a little confusing because everyone is writing different timelines, using different codes and letters, so we want to keep a simple standard for our article.

685

Core idea curated from:

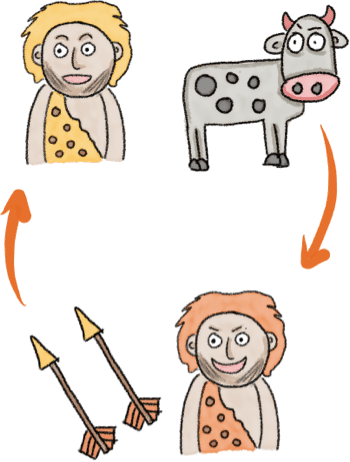

Barter and Gift Economies - 9000 B.C

Bartering is the act of exchanging goods or services without using money, so an example would be: give me 2 arrows and I’ll give you a cow.

Despite the fact that a lot of sources claim that Barter was the first way in which we conducted economical transactions, there is no clear evidence that this was the case and let’s analyse why:

681

Core idea curated from:

Bronze Age - Commodity Money - 3000 B.C

In several places around the world commodity money was gaining traction, now, what do we mean by this?

Well, commodity money are objects that are valuable by themselves and are also valuable when using them as money.

676

Core idea curated from:

The Babylonian civilisation

One of the most interesting parts about this segment of history is that the Babylonian civilisation was already implementing some primitive economic systems where they had contracts, laws, rules of private property and debt.

It was only a matter of time until a universally defined medium of exchange came into play.

678

Core idea curated from:

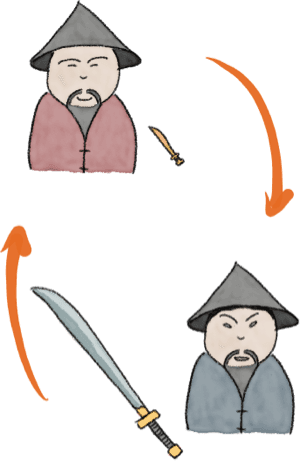

Chinese Miniature Replicas - Around 1100 B.C

Around the year 1100 B.C in certain parts of China miniature bronze replicas of goods were being used, so if you had wanted to get a sword, you would have likely needed to have a miniature bronze sword as the equivalent currency to get one.

Bear in mind that the fact that miniature replicas were being used as currency in China, that doesn’t mean that coins didn’t exist already in some places, they were just not official means of exchange yet.

681

Core idea curated from:

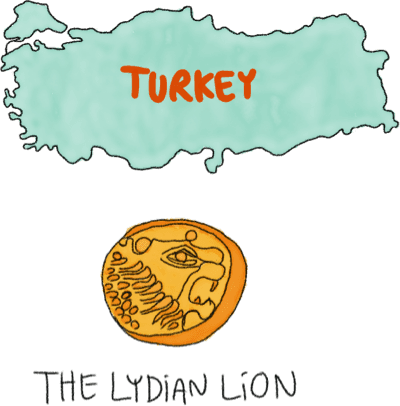

The First Official Currency - Lydian Lion Around 600 B.C

Around 600 B.C King Alyattes minted what would become the first official currency ever recorded.

Each coin was made from electrum alloy which is a mixture of silver and gold.

A very fun thing that we never managed to understand is, why lions were sculpted or depicted with two possible faces:

- Concerned as if they had problems

- Cold as if they were a cartoon freezing

685

Core idea curated from:

The First Paper Money - Around 700 A.D

Around 700 A.D during the Tang Dynasty in China there were already some forms of paper money like bills and credit notes. The Government realised that it was far more convenient to use credit notes to conduct transactions instead of carrying a whole load of coins.

679

Core idea curated from:

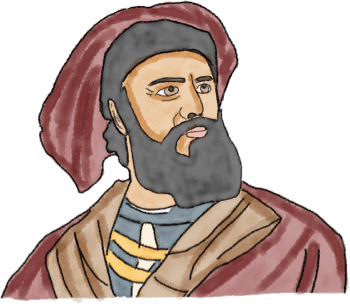

Europe - Paper money

Paper money arrived in Europe thanks to the travels of the great explorer Marco Polo around the year 1200 A.D.

It was not until the year 1661 that the first Banknote was issued in Sweden.

681

Core idea curated from:

The Invention of the U.S Dollar - April 2, 1792

The term "Dollar" already existed before the U.S adopted it as its official currency name. It was very common during the colonial period when referring to the Spanish Real coin.

In the year 1775 the Continental Congress of the United States authorised the issuance of Continental currency but it wasn't until the Coinage act of April 2, 1792 that an official monetary system was defined and the U.S dollar came to life as the official currency for the United States of America.

684

Core idea curated from:

End of the Gold Standard - March 3, 1933 - August 15, 1971

On March 3rd 1933, President Franklin D. Roosevelt closed all the banks in the U.S.A.

Banks held large amounts of Gold which were backing all the available U.S dollars. At those times there was a fixed exchange rate between U.S dollars and Gold.

Gold standard ended officially when president Richard Nixon on August 15 1971 announced that the U.S would no longer convert dollars to gold at a fixed value, that’s how the gold standard ended.

Nowadays, fiat money is no longer dependent on gold but rather on governmental policy.

683

Core idea curated from:

The First Bank Issued Card - Around 1946

The creator of the first bank issued card was Mr. John Biggins of the Flatbush National Bank of Brooklyn in New York around 1946.

Biggins created the “Charge-It” program. Merchants could send sales slips into the bank after a customer used the card with them and the bank would then go and bill the customer back.

674

Core idea curated from:

Frank Macnamara and the Diners Club Card - Around 1950

Frank Macnamara had an idea, to create a card that allowed you to dine in restaurants and the Diners Club would pay your bill and you would pay them later.

The card was originally intended for a very small and exclusive group of 200 people belonging to the club, but the idea caught on fire and in less than a year there were more than 20.000 cardholders and you could use them pretty much everywhere.

675

Core idea curated from:

Paypal and Digital Money - Around 1990

In the 1990’s there were 2 different businesses known as confinity.com and x.com, both were diving into the online banking world separately through several innovative ideas.

At some point both companies decided to merge and gave birth to Paypal, the online payments giant.

Fun fact: Elon Musk the founder of Tesla was the owner of x.com, as you can see, he’s always working on some great thing.

681

Core idea curated from:

Bitcoin and the Crypto Revolution - Around 2009

Around 2009, a mysterious developer known by the Alias "Satoshi Nakamoto" created Bitcoin.

Bitcoin grew with no official employees, no marketing and no investors to become the world’s largest digital currency.

686

Core idea curated from:

Bitcoin

In terms of the history of money, Bitcoin is relevant because it presents the following changes:

- Fiat money is backed by governments, Bitcoin is decentralised and the power lies on the whole network, not one person that can make decisions.

- Bitcoin gave anonymity to people who transact on the network.

- The blockchain system became a way to perpetually store records that cannot be altered and are always publicly accessible.

Thanks to these features, bitcoin took the world by surprise and proposed an interesting leap forward in technology.

691

Core idea curated from:

Life three currencies

- Time: It is a commodity given to every living being, no one has excess or little of it. But it depends on the usage.

- Knowledge: learning does not only happen in classroom but on everyday life.

- Money: it answers all things that pertains to living.

At any given point in your life, you will have at least two of those currencies, and whatever it is you are missing. Use the those two to acquire it.

19

Core idea curated from:

Money Fact

It's true that we have don't understand between LIABILITIES and ASSETS.

Liabilities is the thinge which take out money from you.

Asset is something which puts money in your pocket

10

Core idea curated from:

Economic Indicators

An economic indicator is simply any economic statistic, such as the unemployment rate, GDP, or the inflation rate, which indicate how well the economy is doing and how well the economy is going to do in the future.

Investors use all the information at their disposal to make decisions. If a set of economic indicators suggest that the economy is going to do better or worse in the future than they had previously expected, they may decide to change their investing strategy.

46

Core idea curated from:

Money, Credit, and Security Markets

These statistics measure the amount of money in the economy as well as interest rates and include:

- Money Stock (M1, M2, and M3) [monthly]

- Bank Credit at All Commercial Banks [monthly]

- Consumer Credit [monthly]

- Interest Rates and Bond Yields [weekly and monthly]

- Stock Prices and Yields [weekly and monthly].

41

Core idea curated from:

Financial Intelligence

Financial Intelligence is awareness. Knowing the basics before trying to control them. Do you know what’s your Net Worth? Do you know what’s your Cash Flow? Your Incomes? Your detailed Spending? Do you know what are the interest rates of your liabilities? Do you know your actual hourly wage?

It seems it’s the simplest step one can do, but actually, very few financially-in-trouble people do it. It takes willpower and/or desperation to make the first step. It also requires some knowledge.

59

Core idea curated from:

Financial Integrity

Financial Integrity means taking actions. Once you have a good picture of your situation, it’s usually easy to find and grab low hanging fruits. So, strategies like cutting superfluous expenses come natural and they are easily implemented.

What will happen when you start taking action is that you better define your values. You understand easily that you need to spend less than you earn if you want to get back in financial shape. To do that, you either earn more or spend less (or, better, both).

55

Core idea curated from:

Emergency Fund: Savings 101

You may be enjoying the freedom not having to think about next paycheck brings to your life and start saving, building an Emergency Fund. Eventually, when you have enough cash to survive a year (people recommend 3-6 months) without working, you’ll stop hoarding cash and start investing and/or paying back your debts, sending your money to work for you thanks to the immense power of compounding.

56

Core idea curated from:

Boost Your Earnings

You may also work on the earning side of the equation: once you ‘stash a year of salary you may consider working part time and take some classes or learn a new skill or start a side gig to boost your earnings. You may realize your commute takes too much time and it’s costing you a lot of life energies (opportunity cost) and living far from your office is not worth the few bucks you’re saving.

54

Core idea curated from:

Financial Independence

Financial Independence means tasting freedom. You no long have to work to maintain your lifestyle, since your money are working for you instead. Your passive incomes (like stocks appreciation, dividends, rental properties income,…) cover your living expenses and you’re free to choose what to do.

You may keep your current job, try a different career, go back to school, take entrepreneurial steps, work less, work none. You may have dreams you want to follow, people you want to take care of. It’s really up to you. You’ve got freedom.

60

Core idea curated from:

Freedom From Exchanging Time For Money

Freedom here stands for freedom from selling your time for money. You no longer need it. You’ll rely on your passive incomes robustness, like betting on average market returns of 7% per year (inflation adjusted) on the long run or a combination of good tenants, rent/house appreciations and low vacation rate for your rental properties.

54

Core idea curated from:

Financial Freedom

Financial Freedom means removing money from the equation.

True financial freedom is when you have almost military grade security measures against unplanned events. Rock solid financial integrity with a monthly budget well beyond your most desirable spending regime at your safe withdrawal rate. Or, equivalently, a withdrawal rate of 1% or less at your current spending regime.

No economic event in the foreseeable future (excluding catastrophes, world war or a sudden depletion of earth resources) can put your plan at risk.

56

Core idea curated from:

True Financial Freedom: The Rule Of Free

- Make all spending decisions as if the price were $0.00

- Make all work and income decisions as if the wage were $0.00

58

Core idea curated from:

Less Ego, More Wealth

Saving money is the gap between your ego and your income, and wealth is what you don't see. So Wealth is created by suppressing what you could buy today in order to more stuff or more options in the future.

353

Core idea curated from:

Manage your money in a way that helps you sleep at night.

Some people won't sleep well unless they are earning the highest returns; others will only get a good rest if they're conservatively invested. To each their own.

303

Core idea curated from:

1. Start Thy Purse To Fattening - Start Earning

- Set aside 10% of your income for you!

- You can use that other 90% to pay bills and other expenses. But that 10% is specifically for you to save and invest later on.

- It seems small at first, but gradually, you’ll start to have a good amount set aside.

653

Core idea curated from:

The Five Laws Of Gold

- When you save part of your income (even if you have a low income), it helps you build up your wealth.

- When you invest your money, it will multiply so you have more of it.

- Leverage the advice of financial experts if you need to when investing your money for more security.

- Don’t rush headlong into an investment you know nothing about! It’s just asking for trouble.

- Don’t fall for get-rich-quick schemes or scams. You’ll lose your money.

744

Core idea curated from:

Government response to the Invisible Hand

The lack of market mechanisms frustrates government planning. This is also known as the economic calculation problem.

When people and businesses make their own decisions based on their willingness to pay money for a good or service, the information is captured. In turn, resources are automatically allocated toward the most valued ends.

Governments' interference causes unwanted shortages and surpluses. However, the forces that guide voluntary economic activity toward the benefit of societies are the same forces that curb the effectiveness of government intervention.

20

Core idea curated from:

The elements of prosperity

Smith believed a nation needed three elements to bring about universal prosperity.

- Enlightened self-interest. He thought most people would naturally practice thrift, hard work, and enlightened self-interest.

- Limited government. Smith viewed the government's responsibilities as being limited to the defence of the nation, universal education, public works, the enforcement of legal rights and the punishment of crime.

- Solid currency and a free-market economy. Smith hoped backing the currency with hard metals would prevent the government from depreciating the currency.

21

Core idea curated from:

Money

Prior to the existance of Layered Money there was simply money.

Money is a tool which allows peers the exchange of goods within a consensus value.

276

Core idea curated from:

Forms of Money

Let's see different forms of money used historicaly:

- Seashells

- Animal Teeth

- Jewelry

- Livestock

- Iron tools

And then...

GOLD & SILVER appeared.

281

Core idea curated from:

Gold & Silver Coins

Initialy, gold and silver coins were issued as a first-layer form of money. Which means that coins where backed by its own value depending of the purity of gold/silver contained.

First records of coins usage trace back to around 700 BC in Lydia, modern-day Turkey.

Over the years, each region minted their own coins, which varied in gold/silver purity.

275

Core idea curated from:

Cons of Gold & Silver Coins Usage

Gold & Silver Coins were a huge implementation for humanity growth & evolution. Unfortunately they had some cons:

- Coin Multiplicy: There were too many different currencies, which was an issue to money velocity (how quickly money changes hands).

- Risks of Physical Transfer: sending coins across land and sea was dangerous and a logistical nightmare during the medieval era.

273

Core idea curated from:

"Always and everywhere, monetary systems are hierarchical."

PERRY MEHRLING

272

Core idea curated from:

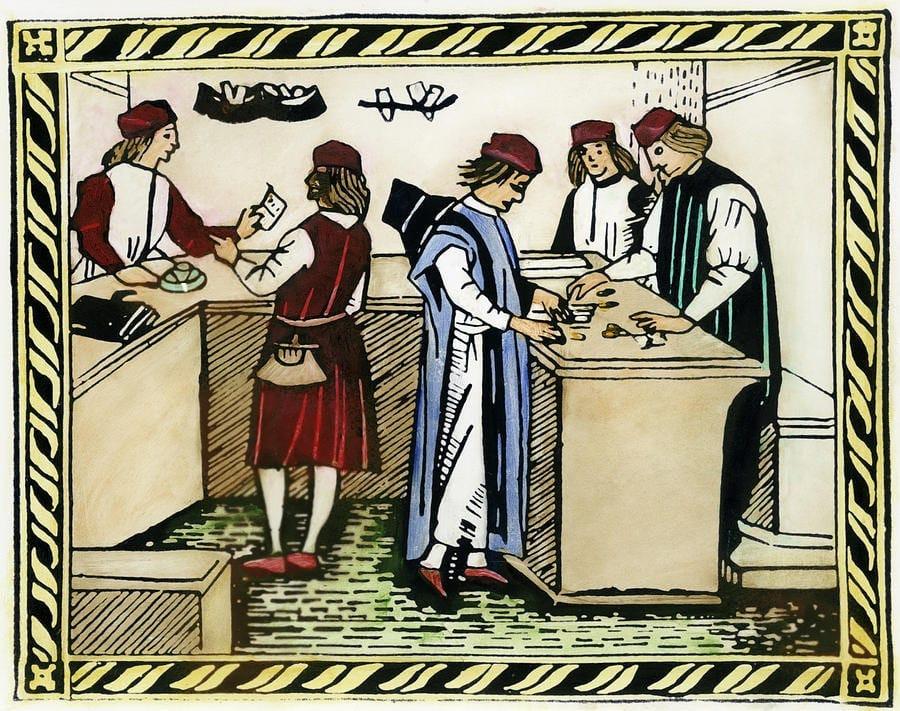

Medici Banking Dynasty

First of all we need to see the difference between first layer & second layer money:

- A gold coin - First Layer Money.

- A piece of paper (bills of exchange) that says: "The Medici banking family will pay one gold coin to the bearer on demand". - Second Layer Money.

The gold coin is a first layer money because it is the basis of the monetary system. If the gold coin wouldn't exist the piece of paper wouldn't neither.

281

Core idea curated from:

Bank of Amsterdam (BoA)

It was created back in 1609 and thanks to the world's first joint-stock company, the Dutch East India Company (Vereenigde Oostindische Compagnie, or VOC).

The VOC was the first example of equity investors providing capital in exchange for a share of ownership in the form of a paper certificate.

As the shares increased in value, original investors wanted to realize gains by selling them for cash to new investors, and that is how the first stock market was born.

All cashiers were forced to surrender precious metal to the Bank of Amsterdam and were issued BoA deposits in return.

289

Core idea curated from:

Bank of England (BoE)

The Bank of England was created in 1694 with the purpose to purchase new government bonds in an effort to rebuild the country after a crushing defeat of the English navy.

It was tasked with taking custody of precious metal, issuing deposits, effecting transfers between depositors, and circulating notes as cash.

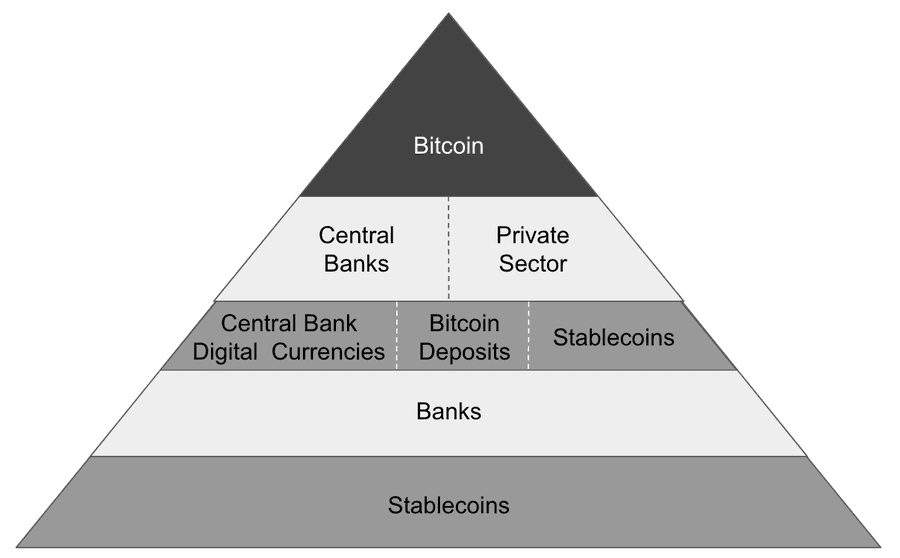

The Bank of England and the Private Sector (private banks/non-government entities) created the third-layer of money.

This third-layer money was issued by Private Sector and its value relied on both BoE Deposits and BoE Notes. Private Sector issued:

- Deposits

- Bills of Exchange

274

Core idea curated from:

"Gold is money. Everything else is credit."

J.P.MORGAN

304

Core idea curated from:

Federal Reserve System

Shortly after an earthquake in 1906 rocked San Francisco, the US immersed into a financial crisis.

Congress passed into law the Federal Reserve System on Decemeber 23, 1913.

The Fed was founded to combat financial crises, and it would do this with a second-layer money called reserves.

Wholesale money (Fed reserves) is money that banks use, and retail money (Fed notes) is money that people use.

280

Core idea curated from:

Federal Reserve Act

The Federal Reserve Act's stated the following purposes:

- To provide for the establishment of Federal reserve banks.

- To furnish an elastic currency.

- Means of rediscounting commercial paper.

- To establish a more effective supervision of banking in the US.

The Act also decreed that at least 35% of the Fed's assets must be held in gold.

279

Core idea curated from:

No Gold for the People

Franklin Roosevelt issued Executive Order 6102 on April 5, 1933 which instructed all "gold coin, gold bullion, and certificates to be delivered to the government."

The order was effectively a forced sale of gold in exchange for Fed notes (cash) by all US citizens and eliminate the people's access to first-layer money.

In 1934 the US devaluated the dollar against gold by increasing the gold price from $20.67 to $35 per ounce.

The goal was to attract foreign demand by having the cheapest prices.

281

Core idea curated from:

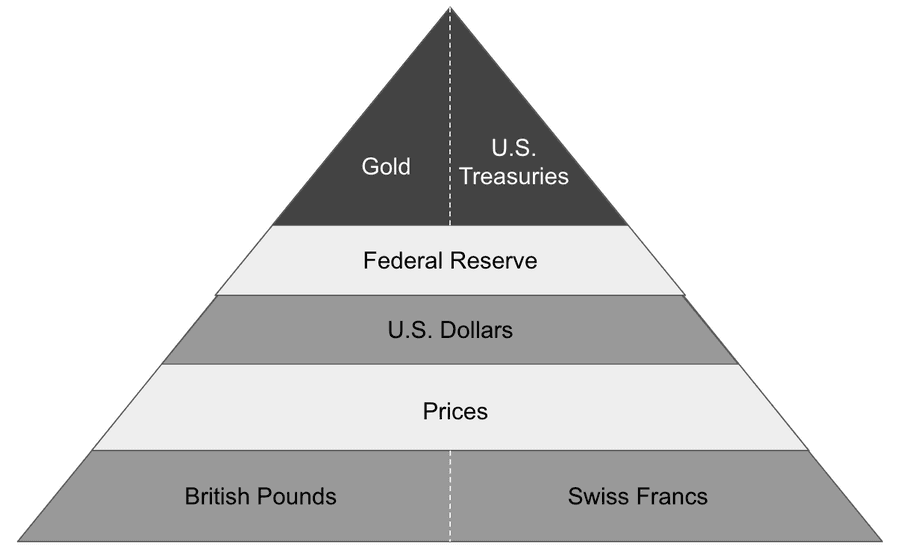

Bretton Woods

In 1944, world leaders gathered at a hotel in Bretton Woods, New Hampshire and formalized that all currencies besides the dollar were forms of third-layer money within the dollar pyramid.

Federal Reserve notes still promised the bearer gold coins on demand at $35 per ounce.

Currencies would have fixed exchange rates with the dollar and wouldn't themselves be redeemeble for gold.

279

Core idea curated from:

Eliminating Gold Convertibility

In 1971, the United States suspended gold convertability for the dollar; the suspension was supposed to be temporary, but the dollar never returned to any linkage with the commodity.

Two years later, the modern era of free-floating currencies began, officially ending the Bretton Woods agreement.

Gold transitioned to the informal role of neutral money, still held today by governments and central banks around the world as first-layer, counterparty-free money.

272

Core idea curated from:

"Today, our financial system is broken. It works, but the fractures within make it prone to ruptures. It almost collapsed in 2008 and again in 2020. The Federal Reserve has done its job as lender of last resort in each circumstance and kept the financial system alive, but everybody now understands the Fed is the world's only true source of liquidity, and without its support the system couldn't stand on its own."

NIK BATHIA

281

Core idea curated from:

A Renaissance of Money

Bitcoin originated back in 2008, forty-six days after the fall of Lehman Brothers. Its whitepaper was sent to a very small online community called the Cryptography Maling List.

The paper was written by Satoshi Nakamoto. The creator remains unknown even now, something that strengthens Bitcoin's neutrality, as no leader exists who wields too much influence, can be coerced or blackmailed, or will try to change Bitcoin's rules.

Satoshi would send his last knwon correspondance in April 2011 and disappeared from the Internet forever.

280

Core idea curated from:

"A puely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial instituton."

SATOSHI NAKAMOTO

276

Core idea curated from:

Defining Bitcoin

It is a completely revolutionary form of money which is characterized by being:

- Immutable and Antifragile.

- Secure and Trustless.

- Transparent and Neutral.

Bitcoin officially refers to two things:

- The Bitcoin software protocol.

- The monetary unit within that software.

Bitcoin uses the Secure Hash Algorithm 256 (SHA256) as security mechanism.

284

Core idea curated from:

Bitcoin Analogies

BTC is digital gold. It's a form of money. People trust BTC because they believe it to be rare and valuable. It has a price in hundreds of different currencies. It doesn't originate from the balance sheet of a financial institution, just like gold doesn't.

BTC is digital land. There are only 57 million square miles of land on Earth. Similarly, there will only be 21 million BTC. This digital land is divisible into the tiniest of parcels.

Bitcoin works similarly to email. Email addresses can be shared with anybody, but only the password holder can access received messages.

278

Core idea curated from:

"The steady addition of a constant amount of new coins is analogous to gold miners expending resources to add goldto circulation."

SATOSHI NAKAMOTO

269

Core idea curated from:

“This is a historical lesson of immense significance and should be kept in mind by anyone who thinks his refusal of Bitcoin means he doesn't have to deal with it. History shows it is not possible to insulate yourself from the consequences of others holding money that is harder than yours.”

SAIFEDEAN AMMOUS

157

Core idea curated from:

Hard Money, Easy Money

Money whose supply is hard to increase is known as hard money (sound), while easy money is money whose supply is amenable to large increases (unsound).

- The easy money trap: anything used as a store of value will have its supply increased, and anything whose supply can be easily increased will destroy the wealth of those who used it as a store of value.

- Money that is easy to produce is no money at all, and easy money does not make a society richer; on the contrary, it makes it poorer by placing all its hard‐earned wealth for sale in exchange for something easy to produce.

156

Core idea curated from:

Time Preferences of Money

Time preference for money is an individual's preference for possession of a given amount of money now, rather than the same amount at some future time. The time preference for money is generally expressed by an interest rate. This rate will be positive even in the absence of any risk. The natural implication of this process is to reduce savings and increase borrowing.

Individuals will consume more of their income and borrow more against the future. This will not just have implications on their time preference in financial decisions; it will likely reflect on everything in their lives.

150

Core idea curated from:

The Importance of Sound Money

- It protects value across time, which gives people a bigger incentive to think of their future, and lowers their time preference (this is what initiates the process of human civilization and allows for humans to cooperate, prosper, and live in peace.)

- Sound money allows for trade to be based on a stable unit of measurement, facilitating ever‐larger markets, free from government control and coercion, and with free trade comes peace and prosperity.

- A unit of account is essential for all forms of economic calculation and planning, and unsound money makes economic calculation unreliable.

150

Core idea curated from:

Money Backed By Gold

- Money has come in all shapes and sizes throughout history, but there’s only ever been one truly sound system: money backed by gold.

- The “gold standard” underwrote an age of prosperity and stability. That all changed in the early 20th century when European governments abandoned gold and fiscal prudence to fund their war efforts.

- The world hasn’t been the same since, and we’ve endured decades of rising debt and boom-and-bust cycles.

- Bitcoin, like gold, it’s a highly effective unit of exchange. But the digital currency will have to overcome some teething problems.

152

Core idea curated from:

The World Before Money

How did it work? It was pretty simple: people just swapped things. It worked fine, except if you didn’t have something your neighbor needed. Once people figured out you could exchange universally valued objects for goods, everything changed.

From there, we’ve gone from all kinds of currency to valuable metals, and now paper printed by governments. But since we ditched the “gold standard” of money and started relying only on easily manipulated paper money, we’ve seen a century of boom and bust and increasing debt.

156

Core idea curated from:

What Makes Good Currency

- What makes good currency is that it is salable or easily sold. With the technology of smelting metals, early pre-Christian civilizations could make highly salable coins that were also extremely portable.

- The preferred type of coin was gold.

- When transportation and communications boomed from the 18th to the 20th centuries, nonphysical forms of payment like paper bills and checks became justified. The way they convinced people to trust these pieces of paper was by backing them with gold.

- Britain led the way with this standard to back bills with gold, known as the “gold standard.”

152

Core idea curated from:

Bitcoin Could Replace Money As We Know It

... because it is scarce, secure, and unique.

- Bitcoin has a fixed supply— there will never be more than 21 million in existence.

- They also have a stable supply because, like gold, bitcoins are mined.

- Bitcoins are the only good defined by absolute scarcity, which makes them immune to manipulation.

- It’s also incredibly secure. The public ledger, known as the blockchain, keeps a record of all recent transactions. Everyone can see it, and it is backed by every computer on the network, making it near-impossible to manipulate.

- The best part is you don’t even need a central authority to oversee it.

152

Core idea curated from:

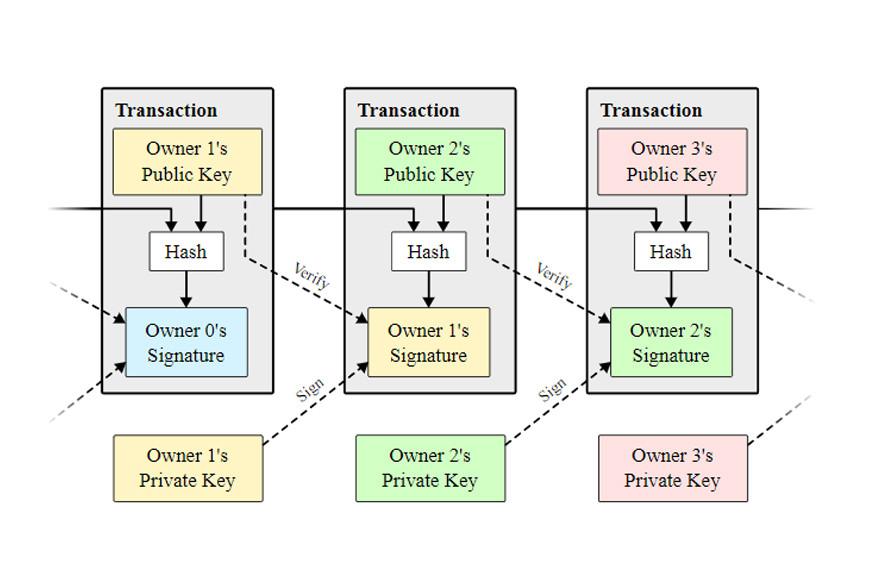

Blockchain and Bitcoin Mining

The Bitcoin blockchain most fundamentally describes a record of transactions simultaneously kept by all peers in the network. Blockchain can be understood as a Distributed & Public Ledger.

Bitcoin mining is the process of verifying new transactions to the Bitcoin digital currency system, as well as the process by which new bitcoin enter into circulation.

For each block successfully mined the winner of the Proof of Work problem of that block gets awarded with 6.25 BTC as an incentive to maintain the blockchain running. This BTC issuance is reduced every 210,000 blocks mined to the half.

277

Core idea curated from:

"The root problem with conventional currency is all the trust that's required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronicaly, but they lend it out in waves of credit bubbles with barely a fraction in reserve."

SATOSHI NAKAMOTO

273

Core idea curated from:

"Actually there is a very good reason for Bitcoin-backed banks to exist, issuing their own digital cash currency, reedemable for bitcoins. Bitcoin itself cannot scale to have every single financial transaction in the world be broadcast to everyone and inlcuded in the block chain. There needs to be a secondary level of payment systems which is lighter weight and more efficient. Likewise, the time needed for Bitcoin transactions to finalize will be impractical for medium to large value purchases."

HAL FINNEY

269

Core idea curated from:

"Bitcoin-backed banks will solve these problems. They can work like banks did before nationalization of currency. Different banks can have different policies, some more aggressive, some more conservative. Some would be fractional reserve while others may be 100% Bitcoin backed. Interest rates may vary. Cash from some banks may trade at a discount to that from others.

I believe this will be the ultimate fate of Bitcoin, to be the "high-powered money" that serves as a reserve currency for banks that issue their own digital cash."

HAL FINNEY

269

Core idea curated from:

Central Bank Digital Currencies

The invention of Bitcoin has changed money forever and forced central banks to respond with their own iteration of cryptocurrency.

Worldwide, central banks are preparing to launch central bank digital currencies (CBDCs) as another second-layer monetary instrument originating from their balance sheets on par with reserves and paper currency.

It's uncertain how CBDCs will be constructed, how similar or different their technology will be to Bitcoin's, or the impact they'll have.

273

Core idea curated from:

Psychology of money: Emotion and money

The most important emotions in relation to money are fear, guilt, shame, and envy.

- Common fears include the fear of not having enough, the fear of looking stupid, the fear of provoking envy, and the fear of being exposed or humiliated.

- You might feel guilty because you have more than your friends, or you haven’t been particularly charitable, or you’ve had money come too easily.

- Shame is one of the most common and powerful emotions associated with money and personal finance. It is a prime reason people avoid doing what they know they should. It's natural to want to avoid exposure in relation to so

mething you're ashamed about.

135

Core idea curated from:

Examples of shameful feelings related to money

- I don’t have enough money.

- I’ve avoided thinking about finances.

- I’ve avoided doing what I’m supposed to do about finances (creating a safety net, planning for retirement, sensible budgeting).

- I’m really ignorant about all of this.

- I spend too much.

- I buy stuff when I’m unhappy.

When you’re filled with shame the natural tendency is to avoid facing whatever is making you uncomfortable. That avoidance itself leads to additional shame and more avoidance.

146

Core idea curated from:

How to harness money emotions

- Emotion isn’t all bad. It tells you what you’re passionate about, and what really matters to you. It makes you feel alive.

- Anxiety isn’t all bad either. Mild to moderate levels of anxiety are motivating. Harness them to tackle what you need to face and know that you will feel better when you’ve done so.

The key is self-awareness. Much of our emotional world is unconscious. But it’s not that hard to access if you know what to look for and have a blueprint for the kinds of emotions and family stories that can influence your personal relationship with money.

121

Core idea curated from:

The Five Laws Of Money

1. Money comes gladly and in increasing quantity to any man who will put by not less than one-tenth of his earnings to create an estate for his future and that of his family.

2. Money labours diligently and contentedly for the wise owner who finds for it profitable employment, multiplying even as the flocks of the field.

3. Gold clings to the protection of the cautions owner who invests it under the advice of men wise in its handling.

4. Gold slips away from the man who invests it in businesses or purposes with which he is not familiar or which are not approved by those skilled in its keep.

33

Daily Doses of Money Facts and More on the Deepstash App

4.8

14,500+ Reviews

App Store

4.6

92,000+ Reviews

Google Play

In Search of Effective Money Management and Financial Planning Facts?

Start thinking more about your Savings with Our Custom Collections of Finance Fun Facts

Learn more about Money & Investments with this collection

How to create and sell NFTs

The future of NFTs

The benefits and drawbacks of NFTs

Learn more about Money & Investments with this collection

Understanding the basics of cryptocurrency

How to store cryptocurrency securely

Risks and benefits of investing in cryptocurrency

Learn more about Money & Investments with this collection

The differences between Web 2.0 and Web 3.0

The future of the internet

Understanding the potential of Web 3.0

Learn more about Money & Investments with this collection

How to make rational decisions

The role of biases in decision-making

The impact of social norms on decision-making

Start 100+ Journeys

Covering over 50 topics

Contribute to Our Collective Quest for Sharing and Learning Fascinating Money Facts & Insights!

Found some Interesting Facts about Money? Stash it and Spread the Word on Deepstash!

Looking to explore even more ideas?

Why not check out related topics:

Check out our latest Stories & Blog Entries

7 min read

As many of us have probably found out the hard way, cramming for an exam in one long and intensive study session generally doesn’t work out so well. It’s not common to be able to retain information, especially on a broad or profound topic, in one sitting. Information is better retained when it is reviewed repeatedly at different intervals.

8 min read

There are many different ways to learn, and each style or method may not suit everyone’s taste. What comes easy for some may prove difficult for others. Fortunately, there isn’t one way of learning that’s the right way for all. We each need to find what works best for us. Some learn best by diving into long study sessions, while others prefer shorter, hyper-focused learning.

10 min read

Imagine a world where education automatically adapts to your unique learning style, making every lesson engaging, effective, and perhaps even fun. Imagine how much easier it would be to retain information and understand complex topics when presented to you in a more personable way, almost as if it were designed specifically for you. This is what adaptive learning platforms and adaptive learning tools accomplish.

8 min read

How often have you whispered to yourself, "I'm going to start exercising," or "I need to find a better job?" We've all been there, whether it's a New Year's resolution or a heartfelt promise we make to ourselves. But the truth is that most of us struggle to turn these dreams into reality. Despite our best efforts, we often find ourselves falling short, needing more motivation to stay on track, and feeling lost in our quest for self-improvement.

Read like a Pro

Save unlimited ideas

Listen to ideas

Start unlimited journeys

Browse through all Ideas, Tips, Facts & Insights

Explore the World's Best Ideas

Join today and uncover 100+ curated journeys from 50+ topics. Unlock access to our mobile app with extensive features.

ALL IDEAS

Learn 7 personal finance rules that can make or break your financial future. From budgeting to compound interest, these money habits will help you secure your financial freedom.

Profit is overrated, Cash flow is the business lifeboat

Budgeting is a very important aspect in one's life and business too. Personally, I think it will be beneficial if this is taught to children as part of their early childhood education. It can support building financial literacy, discipline, awareness and self-control since young.

Ray Dalio’s journey from near-bankruptcy to founding the world’s largest hedge fund, Bridgewater Associates, wasn’t luck—it was built on principles. Today’s insights focus on embracing failure and radical transparency to turn setbacks into systems for growth.

It's time to

Read like a Pro.

Jump-start your

reading habits

, gather yourknowledge

,remember what you read

and stay ahead of the crowd!Replace doomscrolling with 200,000+ curated ideas

Unlock 100+ tailored journeys on over 50 topics

Unlock unlimited listening to all of our ideas

Get rid of all ads

Get access to the mobile app

3M+ Installs

4.7 App Rating

TOP STASHERS

See all stashers

The more one seeks to rise into height and light, the more vigorously do ones roots struggle earthward, downward, into the dark, the deep — into evil.

Lawyer turned Artist Visionary Curator & Gallerist. Empowering self-love and joy through art & words. www.innerjoyart.com 💝 Instagram : dymphna.art

RELATED TOPICS

See all topics

Supercharge your mind with one idea per day

Enter your email and spend 1 minute every day to learn something new.

I agree to receive email updates