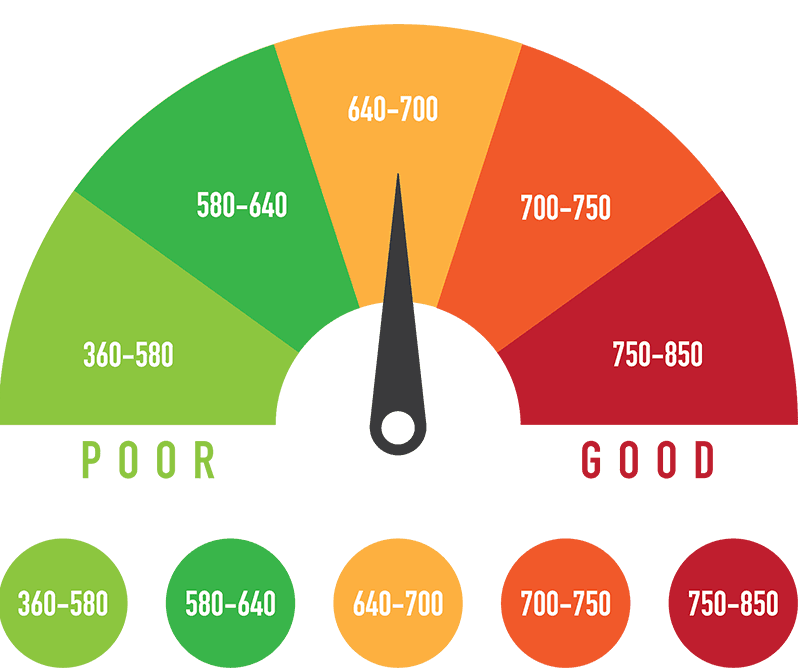

The credit score

It is a three-digit number that lenders use to assess your creditworthiness and your ability to pay your bills on time.

- The score ranges between 300 and 850.

- The higher the score, the more creditworthy you are, and the more likely lenders will lend you money at a lower interest rate.

- The FICO score is the most widely used, but there are also other systems.

- Your history of payments determines your score as well as your credit utilisation.

- Your credit report determines your credit score.

37

209 reads

CURATED FROM

IDEAS CURATED BY

The idea is part of this collection:

Learn more about moneyandinvestments with this collection

The impact of opportunity cost on personal and professional life

Evaluating the benefits and drawbacks of different choices

Understanding the concept of opportunity cost

Related collections

Similar ideas to The credit score

Factors that make up your credit score

- Late or missed payments will drive down your credit score and remain on your record for seven years.

- Credit utilization is the percentage of available credit you're currently using. If you use more than 30% of your available credit, scorin...

Credit scores are different from credit reports

A credit report documents your credit history, your current status of accounts and payments, and when companies have pulled your report when you've applied for credit. A credit report is the source of your credit score.

It is vital to keep an eye on your reports and notice...

Credit repair companies

Common factors that could damage your credit score are negative items, such as bankruptcies, foreclosures, late payments, high credit utilization, and credit inquiries from potential lenders.

Some people employ the services of credit repair companies to dispute incorrect o...

Read & Learn

20x Faster

without

deepstash

with

deepstash

with

deepstash

Personalized microlearning

—

100+ Learning Journeys

—

Access to 200,000+ ideas

—

Access to the mobile app

—

Unlimited idea saving

—

—

Unlimited history

—

—

Unlimited listening to ideas

—

—

Downloading & offline access

—

—

Supercharge your mind with one idea per day

Enter your email and spend 1 minute every day to learn something new.

I agree to receive email updates