How to Save Right for Retirement

- Start Saving ASAP. Money you put in your retirement fund now will have more time to grow through compound growth.

- Avoid cashing out your retirement account early as it prevents your money from being invested and leads to penalties and tax bills.

- Contribute money so your employer can match it if you have a 401(k)

- Invest your raise in your retirement savings. Up your automatic transfer to savings, and increase your retirement contributions.

4.35K

12.2K reads

The idea is part of this collection:

Learn more about moneyandinvestments with this collection

Identifying and eliminating unnecessary expenses

How to negotiate better deals

Understanding the importance of saving

Related collections

Similar ideas to How to Save Right for Retirement

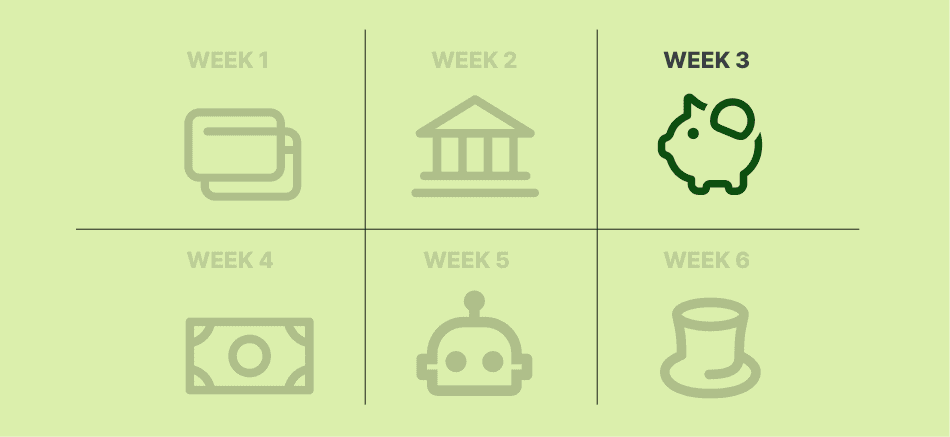

Week 3: Open 2 Investing Accounts

Open:

- a 401(K) account

- a regular investment account.

Next:

- If your employer offers a 401(k) match, invest to take full advantage of it. Contribute enough to get 100 percent of the match.

- Pay off debts. This give you a significant instant return.

Read & Learn

20x Faster

without

deepstash

with

deepstash

with

deepstash

Personalized microlearning

—

100+ Learning Journeys

—

Access to 200,000+ ideas

—

Access to the mobile app

—

Unlimited idea saving

—

—

Unlimited history

—

—

Unlimited listening to ideas

—

—

Downloading & offline access

—

—

Supercharge your mind with one idea per day

Enter your email and spend 1 minute every day to learn something new.

I agree to receive email updates