Here's how to calculate how much money you need 'for the rest of your life' after retire

Curated from: cnbc.com

7

Explore the World's Best Ideas

Join today and uncover 100+ curated journeys from 50+ topics. Unlock access to our mobile app with extensive features.

F I R E

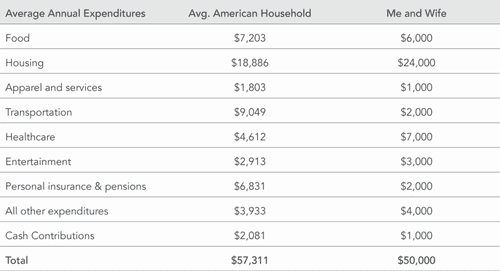

How much money would you need to retire today and never have to work again?

If you’re planning to retire at 65, that figure may seem distant and amorphous. You’re saving as much as you can today so that you can enjoy life as much as possible when you eventually leave your job.

29

677 reads

For adherents to the financial independence, retire early , or FIRE, movement, that figure is much more concrete. “Your FIRE number is the amount of money you need to live on for the rest of your life,” says Grant Sabatier , creator of financial site Millennial Money and the author of “Financial Freedom.”

For many aspiring early retirees, calculating that number comes with an easy shorthand: “The way you calculate your FIRE number is multiplying your expected annual expenses by 25x,” says Sabatier, who reached financial independence at 30 . “Meaning if you spend $40,000 a year, multiplying that $40,000 by 25 would get you to a million dollars.”

30

438 reads

Disclaimer

As with any other one-step financial calculation, the FIRE number math is based on several assumptions and will vary based on your financial situation. Here’s what retirement experts say you need to know to figure out how much money you’ll need to retire.

24

411 reads

The math behind the FIRE number calculation

The FIRE number calculation is rooted in the so-called “4% rule,” which was popularized in an influential 1998 research report known as the “Trinity study.” Included in the research was an examination of past market performance to determine a safe withdrawal rate in retirement.

The conclusion: In 99% of cases, retirees could withdraw 4% per year, adjusted for inflation, from a portfolio of stocks and bonds without running out of money.

When calculating your FIRE number, remember that the multiple of 25 is really just an easier way of dividing by a 4% withdrawal rate. Returning to to Sabatier’s earlier example, if you intend to spend $40,000 a year in retirement, divide by 0.04 to get to your million dollars.

26

339 reads

Additional Notes

As Sabatier points out, some more recent studies suggest it may be wiser to aim for a lower withdrawal rate if you’re hoping for an extended retirement. Researchers at Morningstar peg the safe withdrawal rate at somewhere between 3.3% and 4%, accounting for factors such as relatively low yields in the bond market and relatively high valuations on stocks (which tend to dampen future returns).

If you do calculate your FIRE number and find yourself getting overwhelmed by a huge number, remember that you don’t have to get there all at once, says Sabatier.

24

295 reads

IDEAS CURATED BY

CURATOR'S NOTE

Be prepared for retirement with this simple formula

“

Benny Herlambang's ideas are part of this journey:

Learn more about career with this collection

How to write an effective resume

How to network and make connections

How to prepare for a job interview

Related collections

Similar ideas

2 ideas

5 Key Retirement Planning Steps That Everyone Should Take

investopedia.com

3 ideas

What It Takes to Actually Retire by 30

thecut.com

9 ideas

How to Retire Early | The $50 a Day Early Retirement Strategy

millennialmoney.com

Read & Learn

20x Faster

without

deepstash

with

deepstash

with

deepstash

Personalized microlearning

—

100+ Learning Journeys

—

Access to 200,000+ ideas

—

Access to the mobile app

—

Unlimited idea saving

—

—

Unlimited history

—

—

Unlimited listening to ideas

—

—

Downloading & offline access

—

—

Supercharge your mind with one idea per day

Enter your email and spend 1 minute every day to learn something new.

I agree to receive email updates